Based on standard charging rates from Electric Ireland, the usage of the average amount (4200KwH) makes one pay €1729 annually in Ireland. It contributes to €144/month. Moreover, the expenses on energy bills increase drastically during winter. The only relief is the VAT, which is temporarily reduced from 13% to 9% until 2030.

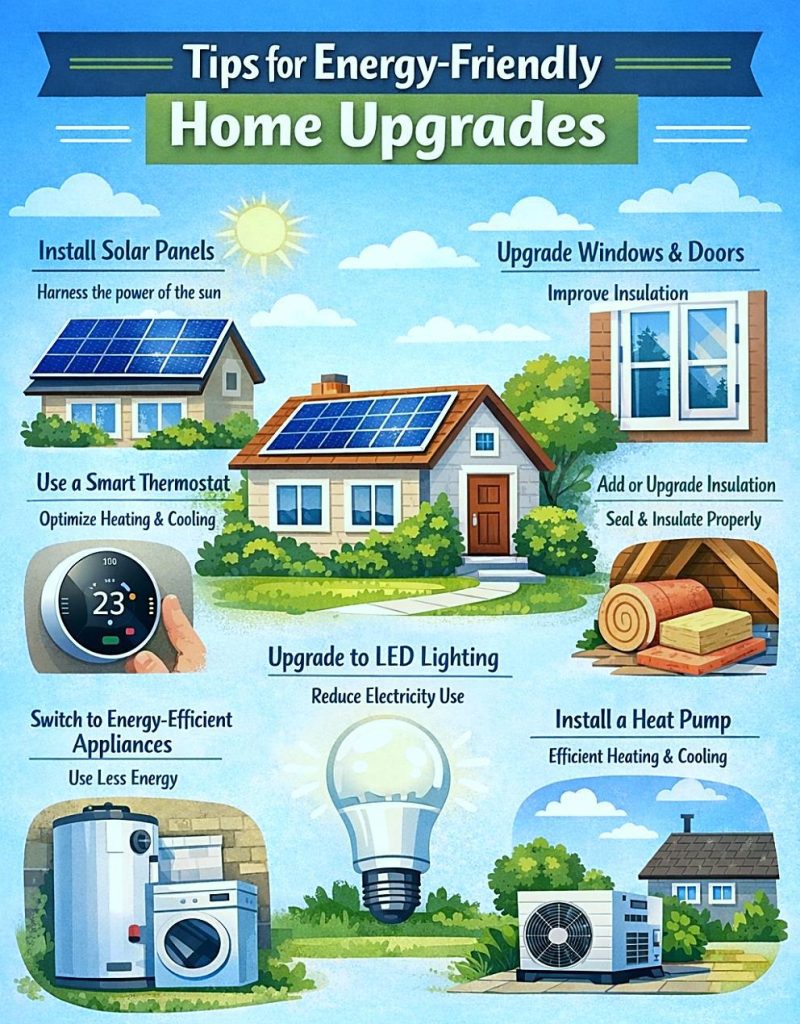

Thus, individuals are looking towards saving some pounds on electricity and other energy expenses. They may consider energy-friendly home upgrades like installing skylights, solar panels, and insulating the home. Such aspects help individuals save money on electricity and other aspects.

For this, they consider the best finance options like green loans and home improvement loans. A green loan is designed to finance environmentally friendly home upgrades like double glazing.

However, a home improvement loan could be used for any value-adding or general home upgrades, like a kitchen makeover, bathroom renovation, etc. These loans could be secured and unsecured, depending on the amount you need and the purpose you need it for. Choosing the right one among these is tricky. The blog discusses which one you should choose for your renovation goals.

Green loan Vs. Home improvement loan: Eligibility criteria

You need to meet the basic criteria to qualify for a green loan and a home improvement loan in Ireland. Both loans vary in usage, and hence, the criteria may differ.

| Who may qualify for a Green loan? | Who may qualify for a home improvement loan? |

| The applicant must be the homeowner or a rental property owner | The house you own must be your primary residence |

| You should possess a SEAI grant permit for energy upgrades. | Should be employed and working consistently for 2 years (at least) |

| 75% of the green energy loan must be used for improvements, and BER must improve by 20% | Credit repayment history with a good payment behaviour in 6 months |

| Must be a regular resident of Ireland. | Should be aged 18-70 as a regular citizen of the country |

Green loan Vs. Home Improvement loan: Maximum Payout

You may get €5000-€75000 for energy home upgrades. These loans come with a repayment term of 10 years. However, the amount you get may vary according to your affordability and the organisation that provides the loan.

For example, you may get up to €75000 if applying with the Home Energy Upgrade Loan Scheme in Ireland for green loans. With credit unions, you may get up to €80,000 for home energy upgrades.

With a home improvement loan, you may qualify for an amount up to €50,000 for any renovation or major upgrade. The amount you get depends on your income, credit score, home equity, and other affordability parameters. Individuals must provide correct documentation and should be clear on the purpose of getting the loan.

Representative example of home improvement loans:

If you borrow €30,000 for bathroom renovation with a repayment period of 45 months, here is how much you need to pay on the loan:

- Monthly payment: €1118.03

- Fixed APR rate: 30%

- Total repayment amount: €50311.14

Green loan Vs. Home Improvement loan: Interest rates

As mentioned above, green loans are designed for home energy-friendly upgrades. Thus, the interest rates on these loans remain more affordable than a home improvement loan. In Ireland, you may get a green loan at an interest rate of 3-6%. It remains consistent and competitive. These are generally variable-rate loans, which means you pay more when the interest rises.

Representative example of green loans

For example, if you borrow €10000 for energy-friendly upgrades like installing solar panels with a variable interest rate of 6.2%-6.4% for 60 months at a monthly instalment of €193.46, the total cost of the loan comes to €11,607.

Alternatively, the interest rates on home improvement loans generally stay fixed. Well, you can also choose variable-rate loans if you want to benefit from the sudden interest drop and save money.

Alternatively, interest rates on home improvement loans in Ireland may vary according to the market and the loan provider’s personal rates. You may get a loan at an interest rate of 6.2%-8.9% (maximum).

However, average interest rates on secured home improvement loans in Ireland is 6%-10%. The interest rate that you get finally depends on the amount, credit score, and loan term that you choose to repay the loan in.

Green loan Vs. Home Improvement Loan: Pros and Cons

Understanding the pros and cons of green loans and home improvement loans may help you finalise your loan choice. Let’s first begin with green loans' Pros and Cons:

| Pros of green loans | Cons of Green loans |

| One may fetch discounts and preferential interest rates on green loans | There is a restriction on fund usage, as one can only use it for energy-efficient home upgrades |

| SEAI grants and tax credits reduce the total expense on loans | May require detailed documentation like- BER improvement evidence, invoices from installers and pre and post-retrofit energy reports |

| The funds are essentially used to improve BER (Building Energy Rating). It thus increases the overall property value. | Lengthy documentation and detailed credit assessment lead to longer approval times. |

| Pros of home improvement loans | Cons of home improvement loans |

| One can use funds for a variety of purposes, like kitchen improvement, bathroom makeover, backsplash repairs, etc. | Interest rates are high on unsecured home improvement loans. Thus, missing a payment may affect a credit score temporarily. |

| Fast fund disbursal and low documentation make it an immediate fetch. You may get quick access to funds for emergency repairs. | It does not offer any discounts, benefits, or tax reliefs, unlike green loans from the government. |

| Interest rates on secured home improvement loans remain low, and one may fetch a higher amount. | One may lose the asset pledged as collateral on a secure home improvement loan in the case of non-repayment or loan default. |

Green loan Vs. Home Improvement Loan: Which one to choose?

Here are some aspects that you can consider to pick the right one between the two.

When should you opt for a green loan in Ireland?

Here are some aspects where a green loan would be the right choice:

- You are carrying out an energy-friendly or decarbonization home project

- You want a loan at low interest rates through schemes like the Home Energy Upgrade Loan Scheme (HEULS) ( starting from 2.99%)

- You are eligible for SEAI grants and have the permit

- You want to improve the BER rating by 20% (minimum)

- Your project qualifies as an energy-efficient upgrade

When should you choose a Home Improvement loan?

Here are some signs that home improvement loans may be apt for you:

- You want to carry out basic home renovations

- You do not qualify for an SEAI permit or a green loan

- You want the loan with minimal documentation and the same day

- You want a predictable monthly payment structure

- You can afford the loan costs

Bottom line

Thus, a green loan is ideal only for energy-friendly home upgrades. You can consider any sustainable home improvement that you wish to benefit from in the long run. The interest rates you get here are lower than those for a home improvement loan.

However, the amount you get on home renovation loans is higher than that of a green loan. You may need to meet certain requirements to get a green loan. However, individuals with good credit history and consistent income may get an instant home improvement loan.