Do you need extra cash but already have a loan? Many borrowers face this same challenge every year. The good news is that most lenders offer options to obtain additional funds. Your choices depend on what type of loan you already have. Car loans work differently from home loans or personal credit.

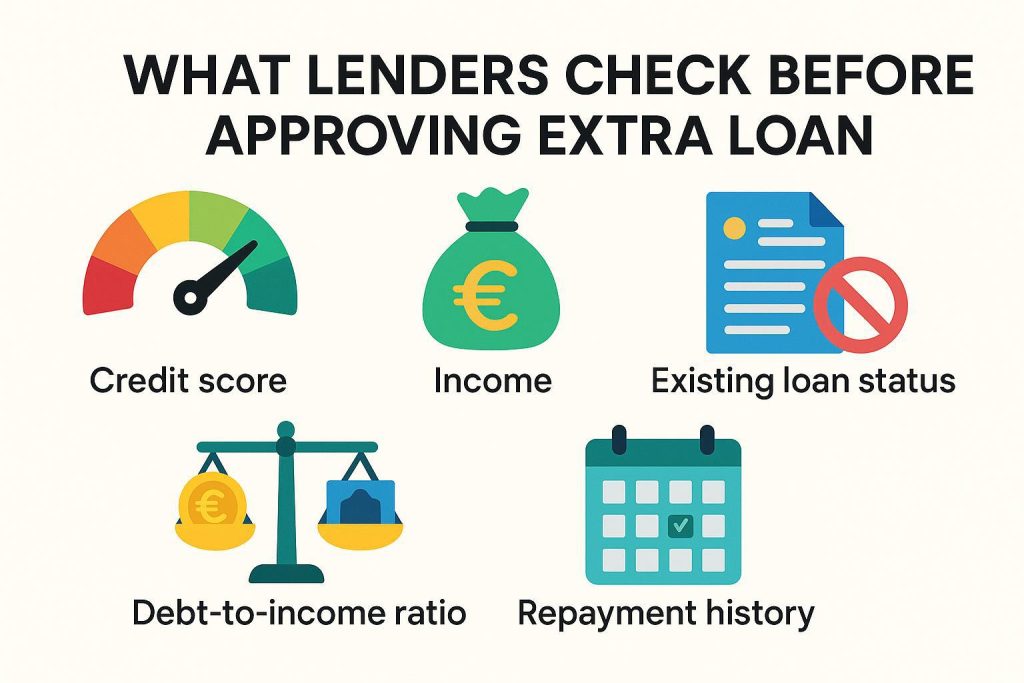

Your credit history plays a significant role in getting approved. Lenders check how you’ve handled your current loan before agreeing to lend you more. They also look at your income to make sure you can pay more. Some small changes in terms can cost or save you hundreds over time.

Can You Top-Up an Existing Loan?

You might not need a new loan. Many banks now let customers add more money to their existing loans. This feature, known as a loan top-up, works like putting extra cash into your existing loan account. It’s becoming a popular way to borrow money in Ireland without the hassle of starting from scratch.

Most lenders review your payment history before approving your loan. Your chances improve a lot if you’ve paid on time for at least six months. They’ll also check your current income and any new debts since your first loan.

The process is often quicker than getting a new loan. You already have a relationship with the bank, so there’s less paperwork and shorter wait times.

- Lower fees compared to starting a new loan

- Keeps all debt in one simple monthly payment

- May qualify for the same or better interest rate

- Often approved within 2-3 business days

- Amounts from £1,000 to £25,000 available

The lender will recalculate your monthly payments based on the new total. You might pay more each month or extend your loan term. You make sure you can handle the new payments before signing anything. Some banks offer free loan reviews to help you decide if topping up makes sense for your money situation.

| Steps to Apply for More on Existing Loan | |||

| Step | Action | Typical Time | Tips |

| 1 | Check existing loan | 1 day | Review balance & term |

| 2 | Assess repayment ability | 1 day | Use the budget calculator |

| 3 | Contact lender | 1–3 days | Ask for a top-up or refinance |

| 4 | Submit documents | 2–5 days | Payslips, ID, and loan statement |

| 5 | Approval & new agreement | 1–5 days | Confirm interest & fees |

Should You Refinance or Restructure Your Loan?

Many people in Ireland choose to refinance when their financial needs change. Refinancing means taking out a new loan to pay off an existing one. This fresh start often includes extra cash for other needs. It’s a smart way to borrow money in Ireland when your credit score has improved since your first loan.

The new loan combines your old balance and any new cash into a single, simple payment. You can pick a shorter term to pay less interest overall. Or stretch it longer to lower your monthly bills when cash is tight.

This move works best when market rates have dropped since you got your loan. A 1% drop can save you hundreds over the course of your life.

- Banks often waive fees for current customers

- Helps fix loans with balloon payments

- Can remove a co-signer from your original loan

- May unlock equity in your car or home

- Offers a chance to switch from a variable to a fixed rate

You can speak with several lenders before making a decision. Some might offer you better terms than you’d receive as a new customer elsewhere. You look for any early payment charges on your old loan. These fees can sometimes eat into your savings from refinancing.

Is It Better to Take a Second Loan?

The second loan maintains your current loan status as is. You simply add a new, separate loan beside it for your extra needs. You won’t get the good terms you may have had on your first loan. This matters if your old loan has a great rate that is no longer offered. Some people also prefer keeping their home and car funds separate from other expenses.

Your income plays the most significant role in getting approved. The lenders will assess your debt-to-income ratio, comparing the amount of debt you have against your monthly income. This debt-to-income ratio helps them decide if you can handle two loan payments.

Most lenders want to see this ratio stay under 40% of your take-home pay. They’ll add up all your monthly bills, including rent or mortgage. Then they check if the new loan would push you past their limit. You’ll likely pay more in total interest compared to a single larger loan. The two due dates can also make your bill planning more tricky.

How Does Credit History Affect Approval?

Lenders review your credit file to understand your financial habits. A clean record shows that you’re likely to repay what you borrow. The lenders first check your current loan behaviour. They require at least six months of on-time payments.

Lenders must check the Central Credit Register for your complete credit history. This system tracks all loans over €500 and your payment pattern on each. They can view five years of your financial transactions at a glance.

The CCR helps lenders spot if you’ve taken many loans recently. You should not apply for multiple loans within a short period, as it may raise concerns among lenders. They worry you might be facing money troubles they can’t see yet. You may receive faster approval or better interest rates than first-time borrowers with a history of on-time payments. Some banks even pre-approve loyal customers for top-ups before they ask.

The new rules in Ireland require credit checks to be more thorough than ever before. Many lenders now see your phone bill and rent payment history. These everyday bills also reveal how you manage your finances.

What Costs and Rates Should You Expect?

The rates can change since your first loan affects what you’ll pay now. If rates have dropped, refinancing could save you money each month. You can keep your old loan; it might be smarter, but if rates have risen.

The total cost depends on how much extra you need. The addition of €5,000 to a €10,000 loan will raise your payments. Many people who borrow money in Ireland often overlook the hidden costs associated with it.

- Admin fees often range from €50 to €150

- Legal costs apply for home loan top-ups

- Some banks charge for early settlement quotes

- Credit check fees may apply with certain lenders

- Ask if the existing payment protection covers the new amount

You receive the full cost in writing before signing. The law requires banks to disclose the total repayment amount to you. This figure helps you compare offers from different lenders clearly.

The best deals often go to those who ask good questions. Don’t be shy about asking what fees can be dropped or reduced. Many lenders will bend to keep good customers happy.

Conclusion

Take the time to run the numbers on each option carefully. You can talk to at least three different lenders to compare their offers. Don’t rush it just because you need cash quickly. Many people regret not shopping around for better terms.

Consider speaking with a free financial advisor before signing anything. These experts can spot issues in loan offers that you might miss. Their advice could save you from costly mistakes. You keep all paperwork safe for later.

Erin Delaney is a financial writer and content strategist with strong hold on personal finance and lending related topics. She is well aware of the fact that talking about money or loans can be stressful for borrowers. To help them make informed financial decisions, she has dedicated her 10 years of her career in making complex topics like loans, bad credit, etc., easy to understand for them.

Her speciality is to write clear, informative and reader-friendly content. She keeps herself updated with the latest trends happening in the lending industry to deliver information that is useful for the borrowers.